The situation is fast-moving, and despite the recent easing of some investor concerns, it definitely still has the potential to turn toxic. Italian public debt outstanding is close to €2 trillion. That is larger than the public debt markets in Germany, France or the UK. In comparison, Greek public debt peaked at around €350 billion in 2011.

Greek default gave the European financial system serious chest pains; but an Italian default would give it a heart attack.

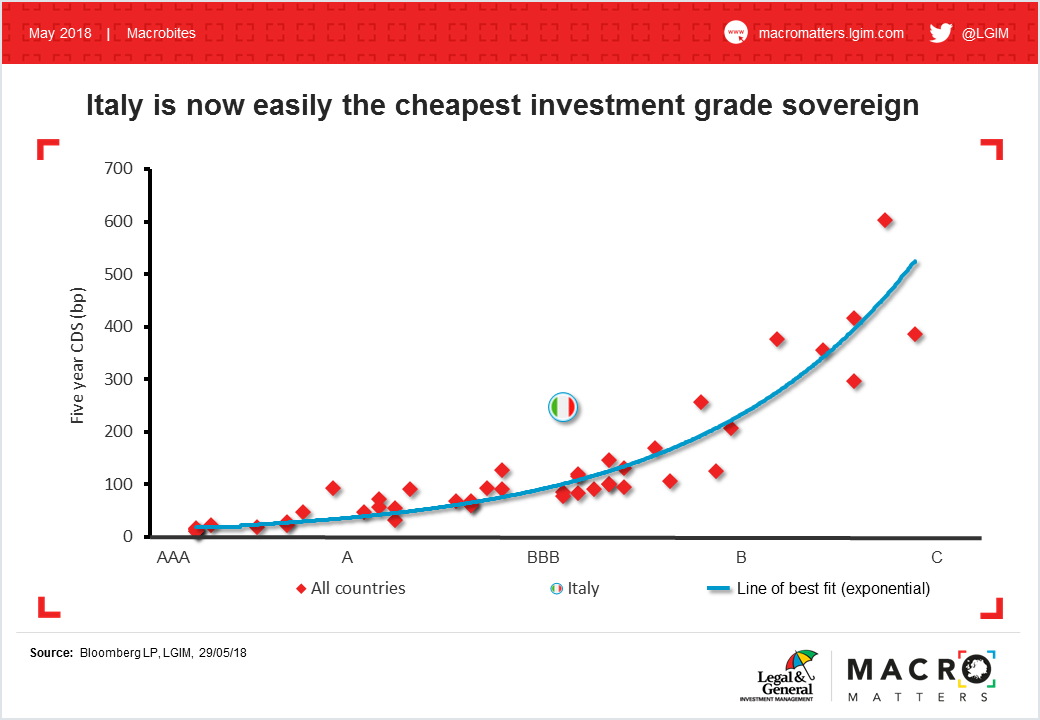

Italy, therefore, looks like an archetypal 'too big to fail' borrower.

However, if Italy were to descend into genuine financial trouble, the European and global bailout funds would be stretched to breaking point. Greece, Ireland and Portugal were locked out of financial markets after their bailouts. The public sector therefore had to assume their gross financing needs for several years and underpin their banking systems.

Italy’s gross financing needs are close to €400 billion per annum. That compares to unused lending capacity for the European Stability Mechanism (ESM), the Eurozone's bailout fund, of €380 billion. Even the International Monetary Fund (IMF) has only around €1 trillion of available resources. For any institution other than the ECB, with its potentially infinite balance sheet, Italy is therefore also 'too big to bail'. Yet the central bank is adamant that for legal reasons, it cannot own more than 33% of a Eurozone country’s outstanding debt – and it already owns around 16% of the Italian debt pile. The monetary guardian also insists that if Italy were to be downgraded to junk by four ratings agencies (Moody's, S&P, Fitch and DBRS), it would have to stop its bond purchases.

So to say the situation is precarious is something of an understatement.

Before letting the deepest and darkest fears overwhelm us, it is worth emphasising how solidly (yes, solidly) Italian finances have been managed in the last few years.

The average primary government surplus of Italy – which excludes debt servicing costs – over the last decade has been +1% of GDP. Of the 35 countries in the OECD, only Norway (due to its vast oil wealth) has been more disciplined. On that measure, Italy’s fiscal prudence has been even stronger than Germany’s.

Similarly, the health of the banking system has improved markedly, with non-performing loans down by over 25% since 2015.

Bulwarks against fiscal craziness are also embedded in the Italian constitution: reforms came into force in 2014 that amended several of its articles with a set of balanced budget provisions. Those are outlined in the box below.

- “The State shall balance revenue and expenditure in its budget, taking account of the adverse and favourable phases of the economic cycle” (art. 81a)

- “Any law involving new or increased expenditure shall provide for the resources to cover such expenditure” (art 81c)

- “General government entities, in accordance with EU law, shall ensure balanced budgets and the sustainability of public debt” (art. 97)

- “Municipalities, provinces, metropolitan cities and regions shall have revenue and expenditure autonomy, subject to the obligation to balance their budgets, and shall contribute to ensuring compliance with the economic and financial constraints imposed under EU law.” (art. 119)

|

Will those defences hold if the government is adamant on blowing things up? We simply don’t know as they have never been tested in the Constitutional Court. But the recent intervention of President Sergio Mattarella suggests he takes his oath to "uphold the Constitution" pretty seriously. It is also worth noting that the septuagenarian president commands significantly more public trust than any other politician, with approval ratings above 65% compared to less than 40% for the party leaders.

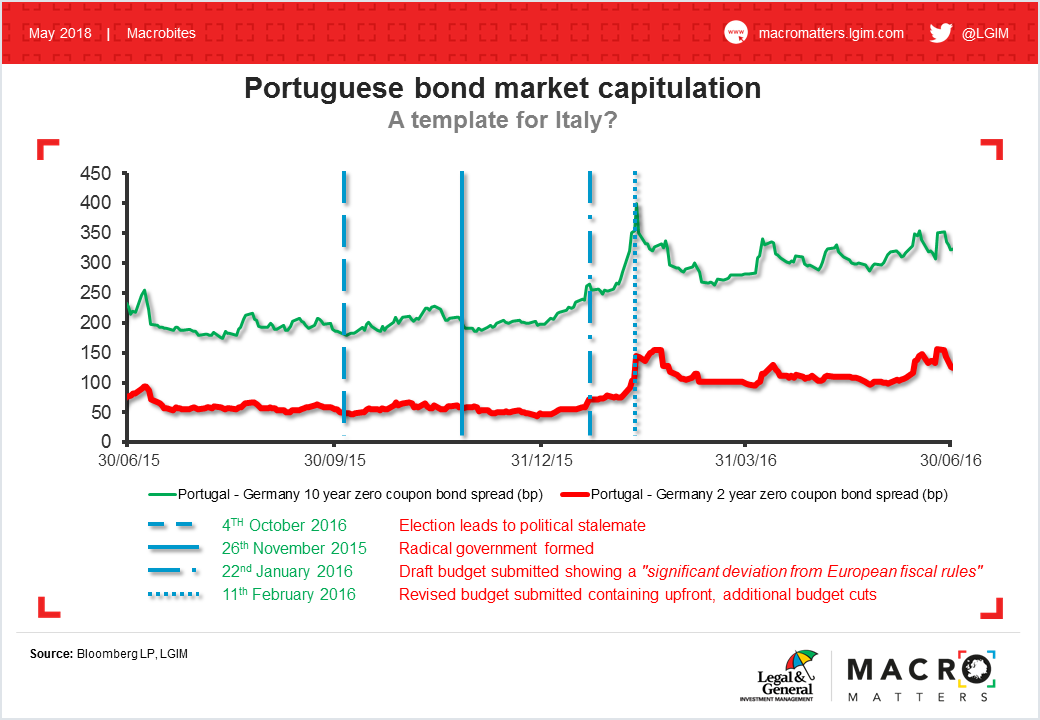

Through all this, we should recall the example of Portugal (see chart below). The Portuguese people elected a government with a radical economic agenda in late 2015; financial stress peaked around three months after the formation of the government. The catalyst for the final blow-up (and subsequent Portuguese capitulation) was a clash with Europe over Portugal’s budget.